This repository contains my personal research notebooks for backtesting pair trading strategies. There are three main notebooks:

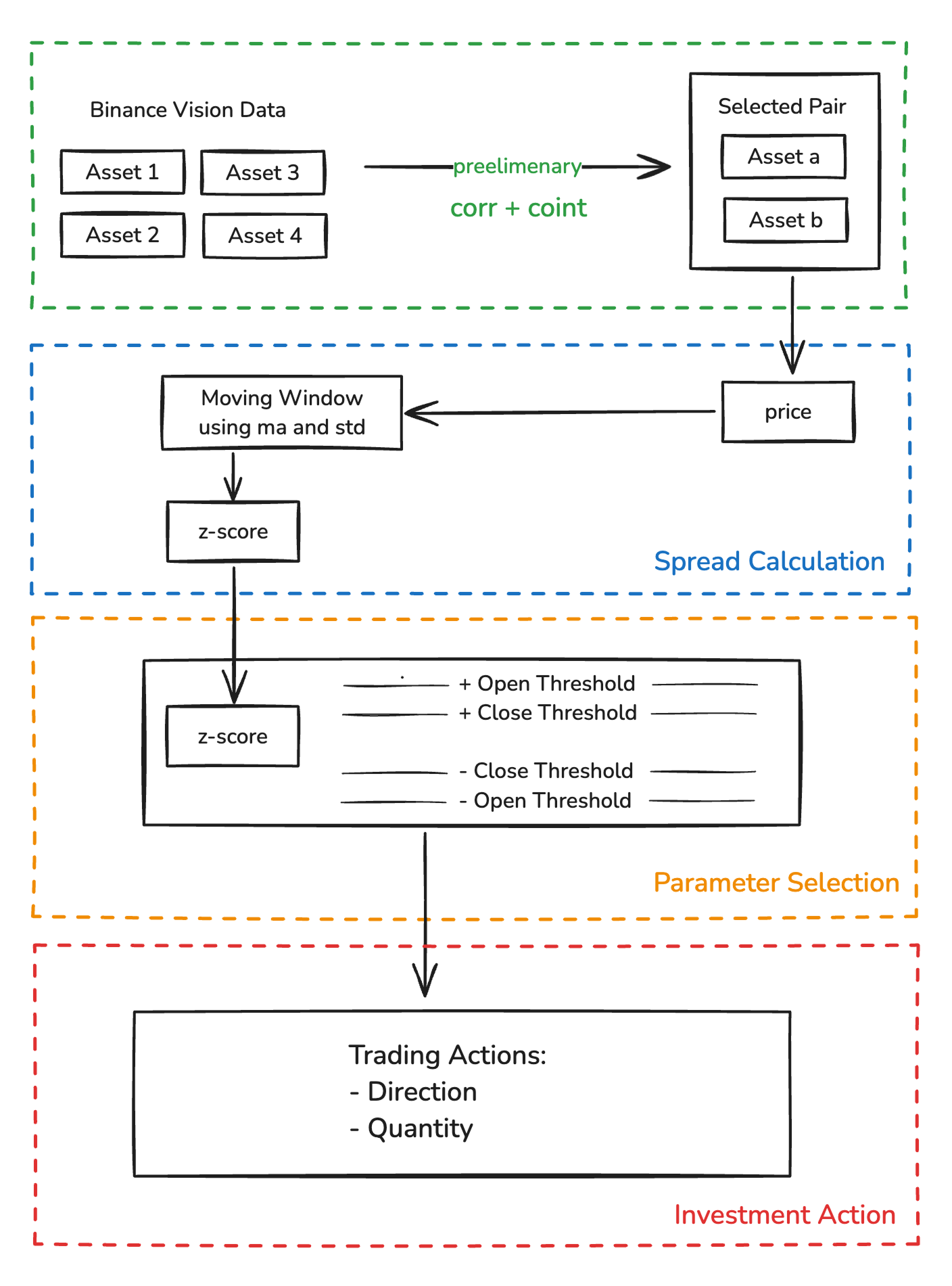

- Preliminaries – Downloads Binance price data and performs cointegration-correlation tests to identify the best pair combinations.

- Gridsearch – Runs backtests and performs a grid search to find the optimal parameters for entry and exit strategies.

- Bidask – Runs backtests while considering bid-ask spreads (incomplete).

To use these notebooks, you will need:

- Python 3.10 (or later)

- Jupyter Notebook

Additionally, make sure to clone the Binance public data repository into this folder:

git clone https://github.com/binance/binance-public-data.gitDon’t forget to create a .env file with the following contents:

BINANCE_API_KEY=

BINANCE_API_SECRET=- Complete the Bidask notebook