Machine Learning Trading Toolkit. Library for portfolio rebalancing strategy research and development.

Modules rewiew:

allocation- Base module for backtesting and strategiesalphas- Experemental formulaic alpha (WorldQuant-like) factor generationdata_loading- Binance and DefiLlama downloader and formattermodels- Implemented strategiesoptions- Pricing binary outcomes (PolyMarket-like)orderbook- Limit orderbook (LOB) feature extractionreport- Risk/Performance reports: metrics, vizualization, etc.technical- Obvious market featuresvalidation- Future leakage checks, strategy testing on subsets of a universecache- Caching backend with modesdata_split- Splitting data into train/val/testutils- Unstructured handy functions and settings

Strategy takes a torch.Tensor input and output is also torch.Tensor

Important note: Sum of absolute values in a row of output weights neet to be

<= 1. Assuming maximum 100% deposit usage and 1x leverage for short selling All the code assumes using log-prices

class CapitalAllocator(ABC):

"""

Abstract base class for capital allocation models.

Capital allocators predict weights for tradable assets based on input data.

"""

@abstractmethod

def predict(self, x: torch.Tensor) -> torch.Tensor:

"""

Predict allocation weights based on input data.

Args:

- `x` (torch.Tensor): Tensor of data. shape: `(>=min_observations, *n_information)` \

`n_information` is number of features. Usually `n_information` = `n_tradable`

Returns:

torch.Tensor: Tensor of predicted weights. shape: `(time_steps, n_tradable)` where time_steps matches input.

Sum of each abs(row) is 1.

"""

pass

@property

@abstractmethod

def min_observations(self) -> int:

"""

Minimum number of observations required for prediction.

Returns:

int: Minimum number of observations

"""

...This example demonstrates a simple time series momentum strategy that takes long positions in assets with positive returns and short positions in assets with negative returns.

import torch

from MLTT import CapitalAllocator

from MLTT.utils import change, to_weights_matrix

class TimeSeriesMomentum(CapitalAllocator):

def __init__(self, lookback_period: int = 252):

"""

Args:

lookback_period (int): Number of days to look back for momentum calculation

"""

self.lookback_period = lookback_period

@property

def min_observations(self) -> int:

return self.lookback_period + 1

def predict(self, x: torch.Tensor) -> torch.Tensor:

"""

Predict portfolio weights based on past returns momentum.

Args:

x (torch.Tensor): Price tensor with shape (time_steps, n_assets)

Returns:

torch.Tensor: Portfolio weights with shape (time_steps, n_assets)

"""

# Calculate returns over lookback period

returns = change(x, lag=self.lookback_period)

signs = torch.sign(returns)

# Normalize to valid portfolio weights

weights = to_weights_matrix(signs)

return weights

if __name__ == "__main__":

# Generate some random price data

n_assets = 3

n_days = 300

prices = torch.randn(n_days, n_assets).cumsum(dim=0)

log_prices = torch.log(prices)

strategy = TimeSeriesMomentum(lookback_period=60)

weights = strategy(prices)

print(f"Portfolio weights: {weights.numpy()}")This strategy:

- Takes price data as input

- Calculates returns over specified lookback period

- Takes long positions (+) in assets with positive returns

- Takes short positions (-) in assets with negative returns

- Normalizes weights to ensure sum of absolute values equals 1

The weights can be used for portfolio rebalancing, with positive weights indicating long positions and negative weights indicating short positions.

All backtest functions assume using log-prices as inputs. This is important for accurate calculation of returns and portfolio performance.

The backtest_model function allows you to test your capital allocation strategies with historical data. This function takes your model and price data, and returns a backtest result with performance metrics.

import torch

from MLTT.allocation import backtest_model

# Create your strategy

strategy = TimeSeriesMomentum(lookback_period=60)

result = backtest_model(

model=strategy,

prices=log_prices,

commission=0.01, # 1% trading commission

save_weights=True # Save portfolio weights for analysis

)

# Access equity curve and other metrics

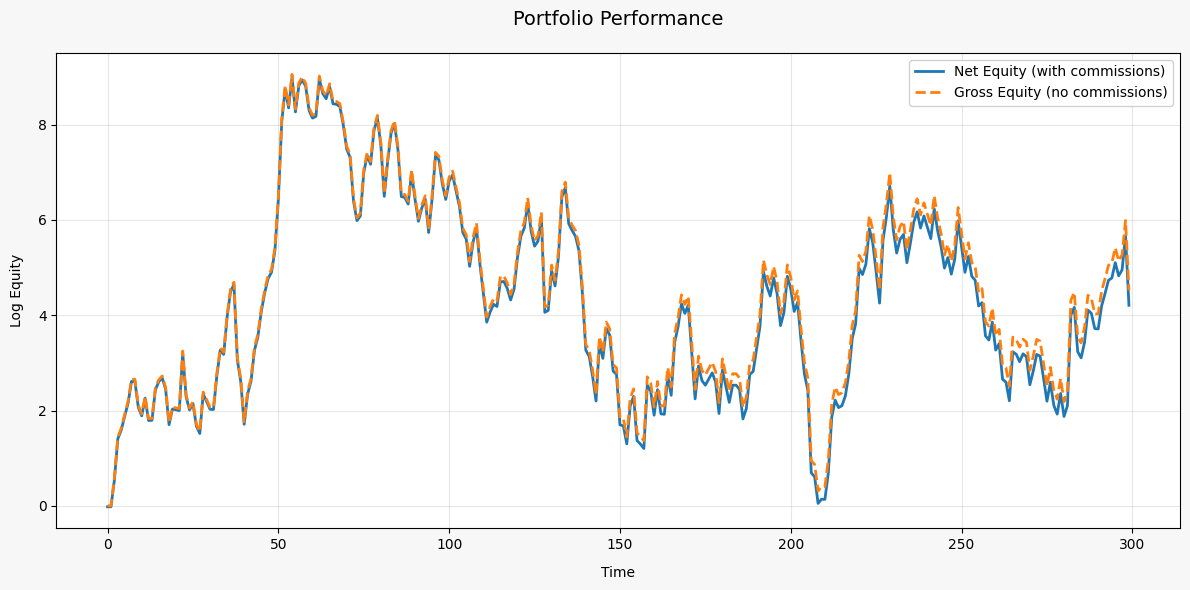

print(f"Final equity: {torch.exp(result.log_equity[-1]).item()}")

print(f"Gross equity: {torch.exp(result.gross_equity[-1]).item()}")

print(f"Total expenses: {result.expenses_log.sum().item()}")Vizualization of result.log_equity and result.gross_equity

You're not limited to using just price data for your strategies. The backtest_model function accepts a prediction_info parameter that allows you to provide custom data to your model:

# Example with custom input data

result = backtest_model(

model=strategy,

prices=log_prices, # Log-prices for calculating returns

prediction_info=custom_data, # Custom data for the model

commission=0.001

)Your custom data can include orderbook information, alternative data sources, technical indicators, or any other features you want your model to consider. This gives you flexibility to develop strategies beyond just using closing prices, such as:

- Market microstructure models using orderbook data

- Sentiment-based strategies using news or social media data

- Multi-factor models combining various data sources

- etc.

Using MLTT.report module you can easily make performance/risk reports for strategies.

from MLTT.report import StrategyReporter

from MLTT.report.metrics import ALL_METRICS, AnnualSharpe, MaxDrawdown, AnnualMean

# Use all available metrics

reporter = StrategyReporter(ALL_METRICS)

report = reporter.compose_report(backtest_result)

# Print report as markdown table

print(report.as_markdown())

# Use specific metrics

custom_reporter = StrategyReporter([

AnnualSharpe(T=252), # Annualize using 252 trading days

MaxDrawdown(),

AnnualMean(T=252)

])

report = custom_reporter.compose_report(backtest_result)

# Get raw values

numeric_report = custom_reporter.compose_report(backtest_result, mode='numeric')

sharpe = numeric_report.values['Annual Sharpe Ratio (Annualization: 252, Risk Free Rate: 0%)']You can create custom metrics by inheriting from the Metric base class:

from MLTT.report.metrics import Metric

from MLTT.allocation.backtesting import BTResult

class CustomMetric(Metric):

@property

def name(self) -> str:

return "My Custom Metric"

def calculate(self, backtest_result: BTResult) -> float:

# Your calculation logic here

return some_value

@classmethod

def format_value(cls, value: float) -> str:

return f"{value:.2f}" # Format as you want

# Use your custom metric

reporter = StrategyReporter([CustomMetric(), AnnualSharpe()])Useful and convinient feature is changing parameters for all metrics:

# Setting timeframe to 1h and risk free rate to 10%/year

reporter.update_all_metrics_params(T=24*365, rf=0.1)Markdown reports by default uses visual mode.

reporter.compose_report(result).as_markdown()Report for all metrics may look similar to table below.

| Metric | Value |

|---|---|

| Annual Mean (Annualization: 1095) | -57.82% |

| Monthly Mean (Annualization: 1095) | -4.82% |

| Annual Standard Deviation (Annualization: 1095) | 45.11% |

| Annual Sharpe Ratio (Annualization: 1095, Risk Free Rate: 2.0%) | -1.33 |

| Annual Sortino Ratio (Annualization: 1095, Risk Free Rate: 2.0%) | -1.43 |

| Annual Calmar Ratio (Annualization: 1095, Risk Free Rate: 2.0%) | -0.96 |

| Maximum Drawdown | 61.99% |

| Average Drawdown | 22.85% |

| Median Drawdown | 23.02% |

| Value at Risk (confidence=95.0%) | 2.34% |

| Conditional Value at Risk (confidence=95.0%) | 3.64% |

| Ulcer Index | 0.27 |

| Skewness | -0.7037 |

| Excess Kurtosis | 9.7834 |

| Average Drawdown Duration | 60d 4h |

| Max Drawdown Duration | 295d 7h |

| Average Position Duration | 6d 9h |

| Daily Turnover (Annualization: 1095) | 18.32% |

The library uses tensor caching by default when running backtests and calculating built-in indicators to improve performance. To manage memory usage, you can use the cache_mode context manager:

from MLTT.cache import cache_mode, CacheMode

# Read-only mode - use existing caches but don't create new ones

with cache_mode(CacheMode.READ_ONLY): # or cache_mode("READ_ONLY")

result = backtest_model(model=strategy, prices=log_prices)Also available caching modes:

READ_ONLYREAD_WRITE- By defaultDISABLED

Cache size can be changed in MLTT.utils

The BucketWatcher module allows you to test strategies on different subsets (buckets) of assets based on some feature or characteristic. This is useful for understanding how your strategy performs across different market segments, such as:

- High vs. low volatility stocks

- High vs. low trading volume assets

- Different beta groups

- Any custom characteristic you can calculate

from MLTT.validation import BucketWatcher

import torch

# Define your feature functions

def volatility(x: torch.Tensor) -> torch.Tensor:

"""Calculate volatility for each asset"""

return torch.std(x, dim=0) # Returns tensor of shape (n_assets,)

def average_volume(x: torch.Tensor) -> torch.Tensor:

"""Calculate average volume for each asset"""

log_volumes = x[:, :, 4] # Assuming OHLCV data

volumes = torch.exp(log_volumes)

return volumes.mean(dim=0) # Returns tensor of shape (n_assets,)

# Create BucketWatcher with price data and optional prediction info

watcher = BucketWatcher(prices=log_prices, prediction_info=ohlcv_data)

# Create buckets based on features

# This will create 4 buckets: top 10% and bottom 10% for both features

indices, names = watcher.make_buckets(

feature=[volatility, average_volume],

quantile=0.1

)

# Test your strategy on different buckets

results = watcher.backtest_buckets(

model=my_strategy,

mode="FILTER_OUTPUT", # or "SUBSET_INPUT"

commission=0.001

)

# Analyze results for each bucket

for name, result in results.items():

print(f"Performance for {name}: {torch.exp(result.log_equity[-1]).item()}")BucketWatcher supports two testing modes:

-

SUBSET_INPUT - The model only receives data from the bucket subset

- Use this to see how your model performs when applied only on a specific subset of assets

- Tests both the model's ability to generate good signals AND how those signals perform on the subset

-

FILTER_OUTPUT - The model receives all data but only the weights for the bucket assets are used

- Use this to see how your model's predictions for specific types of assets perform

- Tests how the model's signals perform on different asset types, but keeps the signal generation process the same

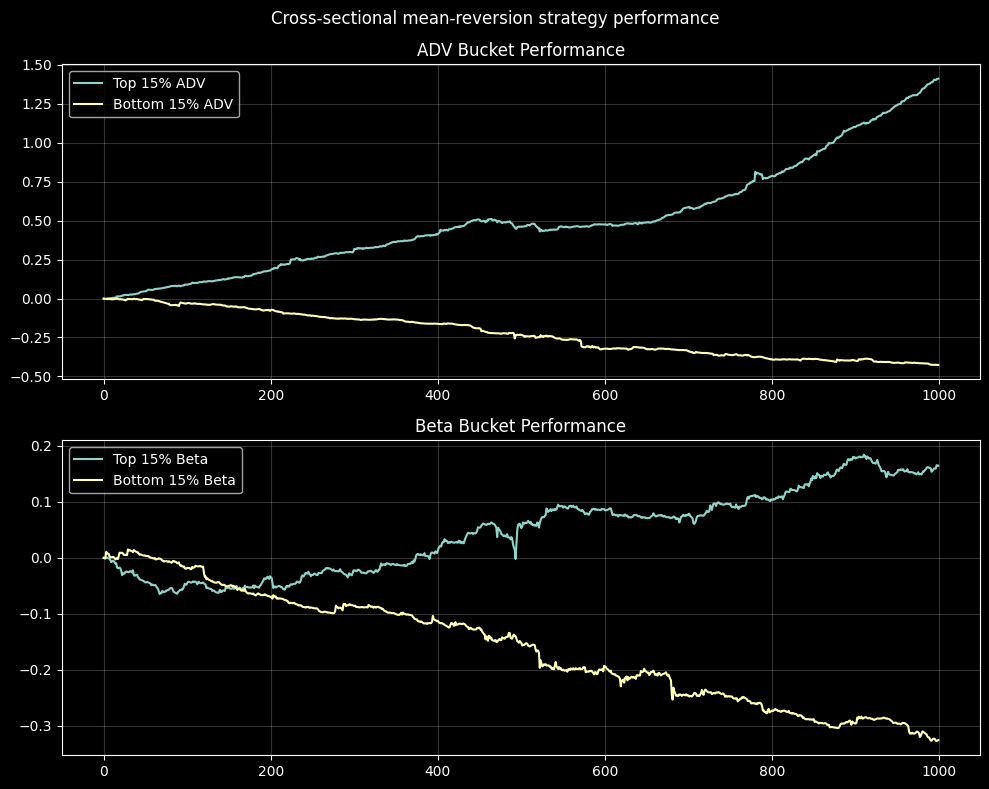

import matplotlib.pyplot as plt

# Plot performance of different buckets

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(10, 6))

# Plot volatility buckets

ax1.plot(results['top_0.1_volatility'].log_equity, label='High Volatility')

ax1.plot(results['bottom_0.1_volatility'].log_equity, label='Low Volatility')

ax1.set_title('Performance by Volatility')

ax1.legend()

# Plot volume buckets

ax2.plot(results['top_0.1_average_volume'].log_equity, label='High Volume')

ax2.plot(results['bottom_0.1_average_volume'].log_equity, label='Low Volume')

ax2.set_title('Performance by Trading Volume')

ax2.legend()

plt.tight_layout()

plt.show()

By analyzing performance across different asset buckets, you can:

- Identify which market segments your strategy works best in

- Discover potential weaknesses or biases in your model

- Gain insights to refine your strategy for better performance

- Create specialized strategies for specific market segments