Risk Overlay #1067

Replies: 4 comments 1 reply

-

|

Here is how you should use the risk overlay (in the relevant blog post and also in the new book):

voila |

Beta Was this translation helpful? Give feedback.

-

|

Thank you. All looks good, but I have a problem: leverage = system.portfolio.get_leverage_for_original_position() Is it something wrong with multiple/adj prices (I use standard csv files)? |

Beta Was this translation helpful? Give feedback.

-

|

|

Beta Was this translation helpful? Give feedback.

-

|

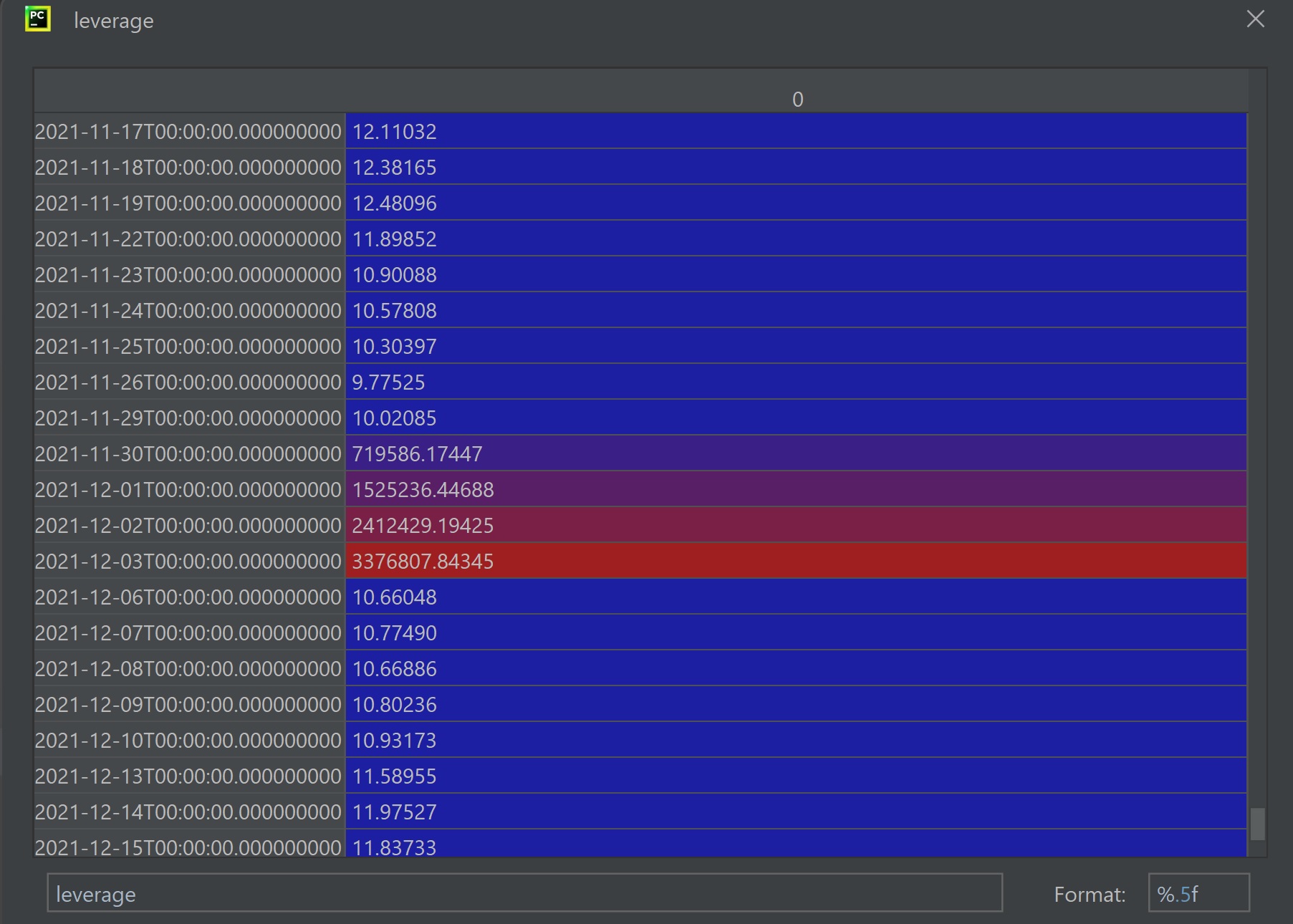

Look at your position plot over time and see if you can work out which instrument is causing that spike I'm afraid I haven't got time to teach you how to debug :-) |

Beta Was this translation helpful? Give feedback.

-

|

Ok, sorry :) I tried different values for risk_overlay, turned it on and off and I always receive the same result. My guess is that risk overlay doesn't work with optimised_portfolio() |

Beta Was this translation helpful? Give feedback.

Uh oh!

There was an error while loading. Please reload this page.

-

Hi all!

I'm backtesting Rob's system with risk overlay and without. And I receive 100% identical annual returns:

annual_return = system.accounts.optimised_portfolio().percent.annual

Is it normal?

Here is risk overlay I added to config.yaml:

risk_overlay:

max_risk_fraction_normal_risk: 1.4

max_risk_fraction_stdev_risk: 3.6

max_risk_limit_sum_abs_risk: 3.4

max_risk_leverage: 13.0

Beta Was this translation helpful? Give feedback.

All reactions